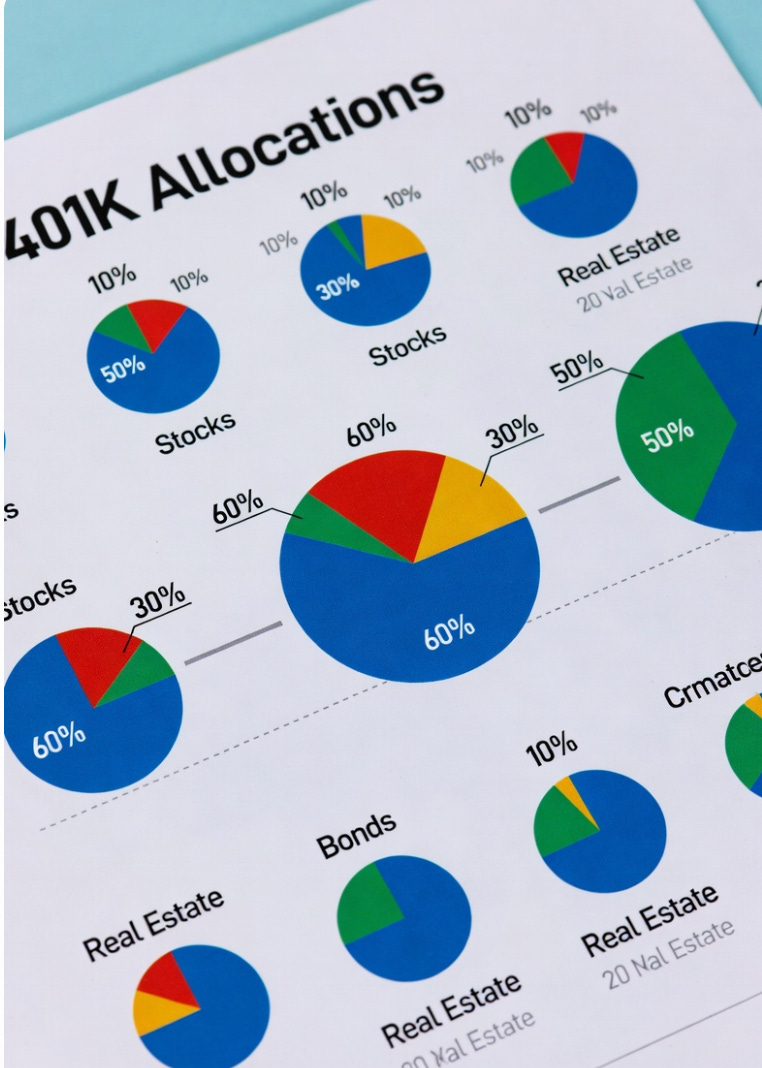

401(k) Asset Allocation: How We Build the Long-Term Pile

401(k) accounts are one of the largest piles most people will ever build… and yet most investors treat them passively, randomly, or emotionally.

The disciplined framework we use to allocate retirement capital across US stocks, global markets, bonds, and real assets