Anatomy of a Trade: Our QQQ Covered-Call Weekly Income Program ($3,500 in Profits)

Both Long Synthetic CC and the Poor Man`s CC. (PMCC)

The full recap · May 29 – July 16, 2026

We just closed the book on one of our best teaching campaigns of the summer — the QQQ covered-call program. For seven weeks we ran two premium-selling structures side by side, rolled them relentlessly, and today we wrapped them up. Here’s the whole thing, start to finish, and the result.

First, the plain-English version of what these are. A traditional covered call means owning 100 shares and selling a call against them for income — like renting out a stock you own. The catch is that 100 shares of QQQ ties up a lot of cash. So instead of buying the shares outright, we used two cheaper “stock replacements”: the PMCC (a poor-man’s covered call — a deep long-dated call, or LEAP, that behaves like the stock at a fraction of the cost) and the synthetic covered call (a long call + short put that together mimic owning the stock). Against each of those cores, we sold a weekly call and rolled it every few days — collecting rent, over and over. Same idea as a covered call, far less capital, and a lot more teachable.

What we ran (the very short version)

May 29 — Opened the PMCC. Bought a long-dated Dec-18 610 LEAP as a stock-replacement core, and started selling weekly calls against it.

June 5 — Opened the Synthetic Covered Call. Built a synthetic long (long Jul-17 717 call + short 717 put) and sold weekly calls against that one too.

May 29 → July 16 — Rolled, and rolled, and rolled. As QQQ ran to record highs and then chopped back, we rolled the short weekly calls 21 times — collecting fresh premium every few days, up and down, week after week.

July 15–16 — Closed both. We took the PMCC off, then closed the synthetic and replaced it with a single, cleaner naked put (same thesis, easier to follow).

Three lessons worth keeping

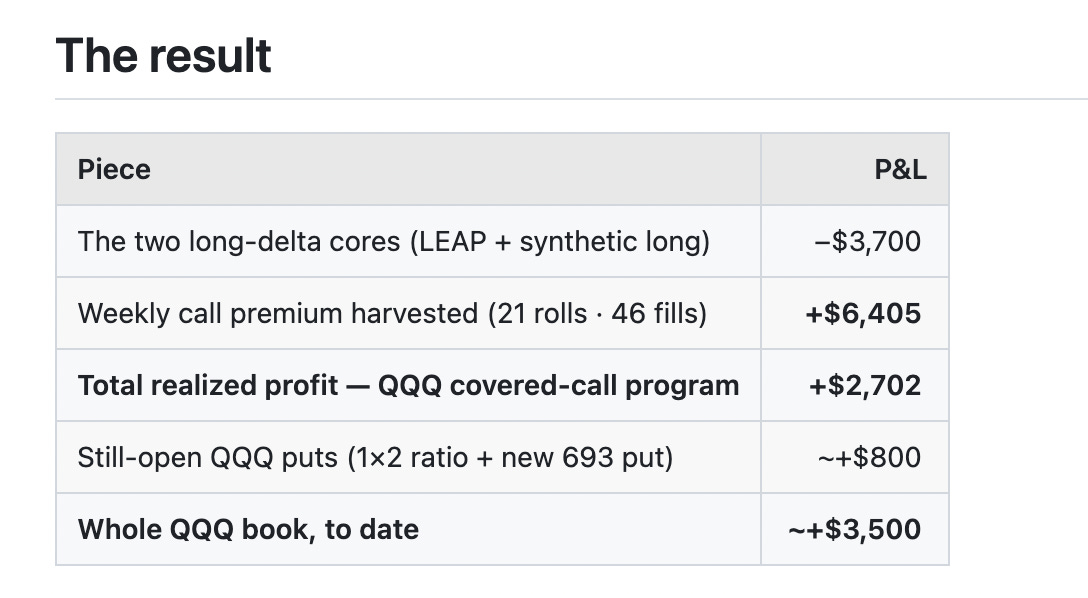

1. The premium engine — not the direction — did the work. Here’s the part that surprises everyone: both of our long-delta cores actually LOST money (about −$3,700 combined) as QQQ ran up and then chopped back. It didn’t matter. The weekly premium harvested +$6,405 — more than enough to cover the cores’ decay and leave a clean ~$2,700 profit. We were never trying to nail the direction. We were collecting rent, week after week, and letting the math work.

2. Discipline beats prediction. Twenty-one rolls in seven weeks isn’t exciting — it’s mechanical. Up days, down days, records, pullbacks; we just kept rolling the short call and taking in premium. That’s the whole edge: small, repeatable, unglamorous, done relentlessly. Duration over direction.

3. Simpler is often better. We finished by replacing the multi-leg synthetic with a single, cleaner naked put — same bullish thesis, far easier for you to follow and learn from in real time. A big lesson in options is that many strategies are synthetically equivalent; once you see that, you stop memorizing recipes and start thinking in risk, Greeks, and probabilities.

The best part? We’re not done — we’re already rebuilding the QQQ premium engine with those laddered naked puts. Onto the next one.

Not investment advice. This is a recap of trades in our own model Portfolio 2, shared for education — not a recommendation. Options involve substantial risk and are not suitable for every investor. Past performance does not guarantee future results.

Want to follow every trade live? Subscribe at growyourpile.com.

— Tony Battista & Tony Rihan