Invitation: GYP Office Hours: The Black Swan Hedge Series — Session 1 of 3

Learn about the most effective Tail-Risk Protection Strategies available to you

How a Famous Hedge-Fund Made 3,612% in 30 Days.

We’ll Build the Retail Version Live This Friday.

🗓 Friday, May 22 · Session 1 of 3

🕕 5:00 PM Eastern · 4:00 PM Central · 2:00 PM Pacific

Announcing the GYP Black Swan Hedge Series

Black Swan hedging is too big a topic for a single Office Hours session. Most traders walk away from a one-hour explanation with a vague sense that “yes, hedging is important” but no actual ability to build a hedge that works.

So we’re not doing that.

We’re spending three full Office Hours sessions breaking down exactly how the world’s best tail-risk funds (Universa, Ambrus Capital, Spitznagel-style operators) structure their crash insurance — and how to build the retail-accessible version yourself.

Why We’re Spending Three Sessions on This

In March 2020, while the S&P 500 lost 30% in twenty-three trading days, Mark Spitznagel’s Universa Investments turned in a 3,612% return on their flagship Black Swan Protection Protocol.

Not 36%. Not 361%. Three thousand six hundred and twelve percent.

So what were they actually doing?

Universa’s protocol is built on deep out-of-the-money put options on the S&P 500 — convex tail-risk structures that cost very little in calm markets but explode in value during crashes. They size the position as a small percentage of the portfolio (single-digit percent), buy continuously, accept the slow drag in calm years as the cost of insurance, and harvest aggressively in the 1-2 day window when implied volatility peaks during a crash.

That’s it. No black box. No quantitative magic. Just deep-OTM puts, sized smartly, held continuously, and harvested at the right moment.

When SPX crashed 30% and VIX hit 80+ in March 2020, those deep-OTM put structures gained thousands of percent — hence the 3,612%. They didn’t predict March 2020. They were positioned for it. That’s the difference between traders who survive a crash and traders who don’t.

The same structural foundation Universa uses is exactly what we teach in our BSH program — just scaled to institutional size with their proprietary refinements. Spitznagel literally wrote a book about the principle (Safe Haven: Investing for Financial Storms). Nassim Taleb is the advisor. The math is public. The structures are public. The discipline is public.

So why doesn’t every premium seller run one?

Two reasons:

1. Most premium sellers think hedging is “wasted money” — until the day it isn’t.

2. Even the ones who want to hedge don’t know how to structure the trade so it actually pays off when it matters.

That’s what the three-part series fixes — in depth, with the time to actually teach it.

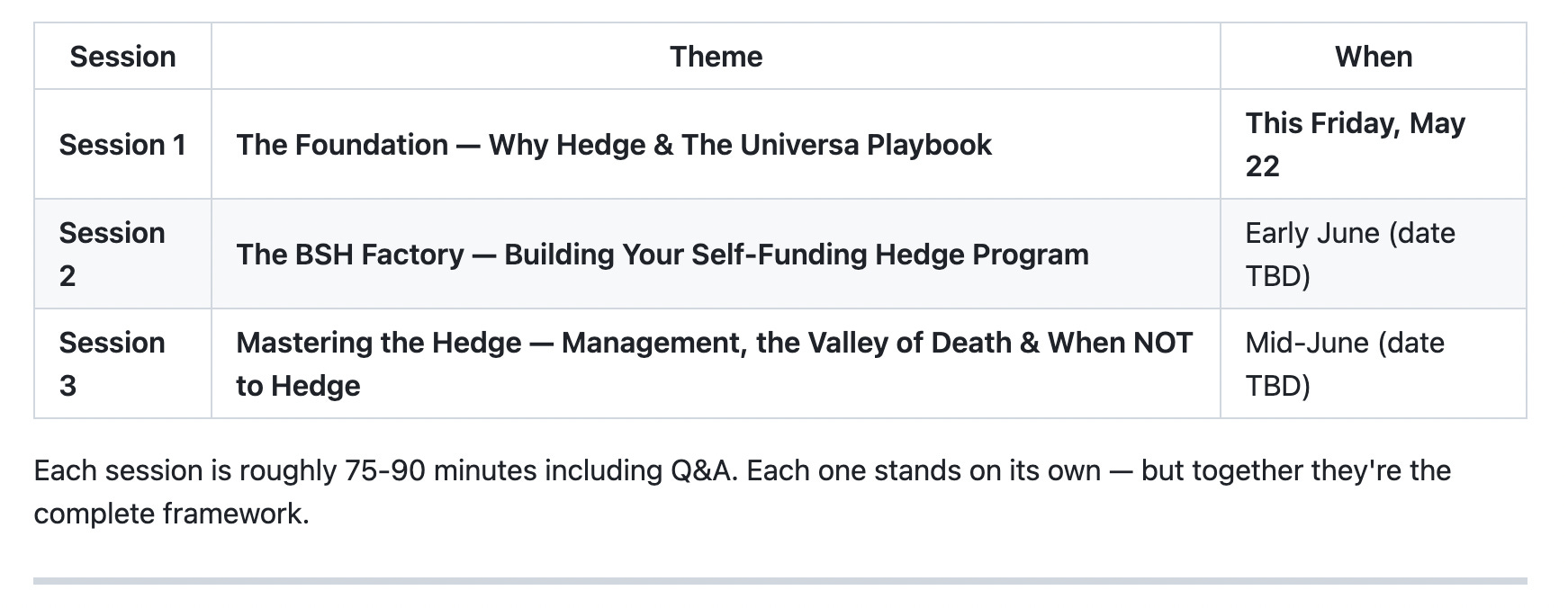

Session 1 — What You’re Going to Learn This Friday

This first session is the foundation. We answer why hedging works mathematically, why even the best premium sellers in the world spend 2-4% of their portfolio every year on insurance they hope they never use, and how the institutional benchmark (Universa) actually does it.

✔️ The math you can’t argue with — why a 50% drawdown requires a 100% gain to recover, the recovery-time table at every common drawdown level, and the difference between arithmetic and geometric returns that determines whether you compound wealth or compound losses.

✔️ The two structural mispricings on the volatility surface — the Volatility Risk Premium (what we harvest selling premium) AND the Tail Premium (what Universa harvests buying tail protection). Both are real. Both can be combined. Most traders only know about one.

✔️ The Universa deep dive — exactly what Mark Spitznagel and his team actually do. The delta zones they target (−0.02 to −0.10), the DTE windows they use (90-180 days primary, up to 2 years on some legs), the rolling cadence (monthly, mechanical, no market timing), and the portfolio allocation framework (3.33% of portfolio, 2-4% annual cost budget).

✔️ The convex structure family — introduction to long puts, put spreads, and the 1/2 ratio backspread that forms the foundation of every convex tail hedge. We’ll walk through the payoff geometry, why convexity matters more than expected value, and how to think about “shape” instead of “average return.”

✔️ The deep-OTM trap most retail hedgers fall into — buying tail puts so far out of the money they wouldn’t pay off even in a real crash. We’ll cover the actual delta zones that protect you vs the lottery-ticket strikes that just expire worthless.

✔️ Why now matters — the May 19 rates-driven pullback was a regime warning. Stocks down + bonds down = a different kind of stress than 2008 or 2020. We’ll cover why your existing hedges might not be doing what you think they’re doing.

What’s Coming in Sessions 2 & 3

Session 2 — The BSH Factory (early June)

Now that you understand why hedging works, Session 2 is how to build a self-funding hedge program at retail scale. The 1/2 and 3/5 BSH structures in deep detail. The Factory Model — how harvested short-put premium funds ongoing hedge purchases until the program pays for itself within 6-12 months. Sizing rules per portfolio size. Regime-based deployment (when to buy, hold, harvest). Real crash payoff numbers from Aug 2015 ($600K), Feb 2018 ($233-290K), and March 2020.

Session 3 — Mastering the Hedge (mid-June)

The hardest part of running a hedge program isn’t building it — it’s NOT cutting it at the worst possible moment. Session 3 covers the Valley of Death (the price zone where shorts hurt but longs aren’t yet convex, where most hedge programs die from trader psychology, not bad math). The three conditions you need to see before adjusting mid-crisis. The five exit rules. Delta speed triggers for mechanical hedge sizing. The common mistakes — including the deep-OTM trap, rolling in the valley, and selling hedges right before they pay off. Plus multi-asset complements: VIX call spreads, tail ETFs (TAIL, CAOS, SWAN, BTAL), defensive sector rotation, and the regimes where bonds STOP working as a hedge.

We’ll close the series with live Q&A integrating everything from sessions 1, 2, and 3.

After Each Session — The White Paper

Within 24 hours of Session 3 (the final session in the series), every attendee — and every GYP subscriber, free or paid — will receive the GYP Tail Risk Hedging White Paper.

This is the deepest, most thorough reference document we’ve ever put together. Thirteen full sections covering every option-based, ETF-based, and multi-asset tail hedge currently available to retail traders, plus the framework for choosing among them, plus the full Universa methodology breakdown.

It’s deeper than anything in our 12-module Masterclass. It’s the document we want every paid GYP member to have on file as a permanent reference.

You don’t want to miss it.

Submit Your Questions Ahead of Time

This is a deep series. The more specific your questions, the better the answers.

For Session 1 specifically, send questions about:

The math of hedging vs the cost of hedging

How Universa-style strategies actually work mechanically

Whether tail protection makes sense for your account size

Why your current hedges (if any) might not be doing what you think

The difference between insurance, lottery tickets, and convex structures

For Sessions 2 and 3 — questions about BSH mechanics, Factory Model implementation, and Valley of Death management — we’ll collect throughout the series.

Why This Session Matters Even More Right Now

The last six weeks have been one of the most powerful momentum rallies in recent memory. SPX broke out, the FOMO chase began, and most traders forgot that markets actually pull back.

This week we got the first real two-day pullback. Stocks down, bonds down, rotation into defensives, small caps leading lower. Yesterday I wrote about why this is a rates problem not a recession scare — and why the textbook 60/40 hedge isn’t working when both halves sell off together.

That’s the kind of market that demands an answer.

If you’ve been running premium sales naked or with under-built hedge protection, now is the moment to learn this — not after the next 10% drawdown. Markets don’t ring a bell at the top. They gap down on a Sunday night.

Why You Should Be There — All Three Sessions

The Volatility Risk Premium is real. It’s how we make money week in and week out selling premium.

But there’s a second structural premium most traders never even hear about — the Tail Premium. Investors systematically underpay for far-out-of-the-money protection. That mispricing is what Universa harvests in crashes. And it’s exactly what we want our subscribers to know how to harvest too.

The hedge isn’t the opposite of premium selling. It’s the complement. They feed off opposite sides of the volatility surface. Both edges are real. Both can be harvested. The traders who combine them are the ones who survive over decades — not just months.

Over three sessions, we put the whole picture together. Session 1 starts Friday.

👉 Session 1 is free for paid subscribers Only.