P2 — The QQQ - Long Synthetic and PMCC Covered Calls: A Full Recap

We run two different QQQ covered-call structures in Portfolio 2 — and with our covered-call Office Hours coming up, this is the perfect moment to lay both of them out.

A roll-by-roll look at our two QQQ income trades

We run two different QQQ covered-call structures in Portfolio 2 — and with our covered-call Office Hours coming up, this is the perfect moment to lay both of them out, every roll, with the real numbers. No cherry-picking: here’s exactly what each trade has done.

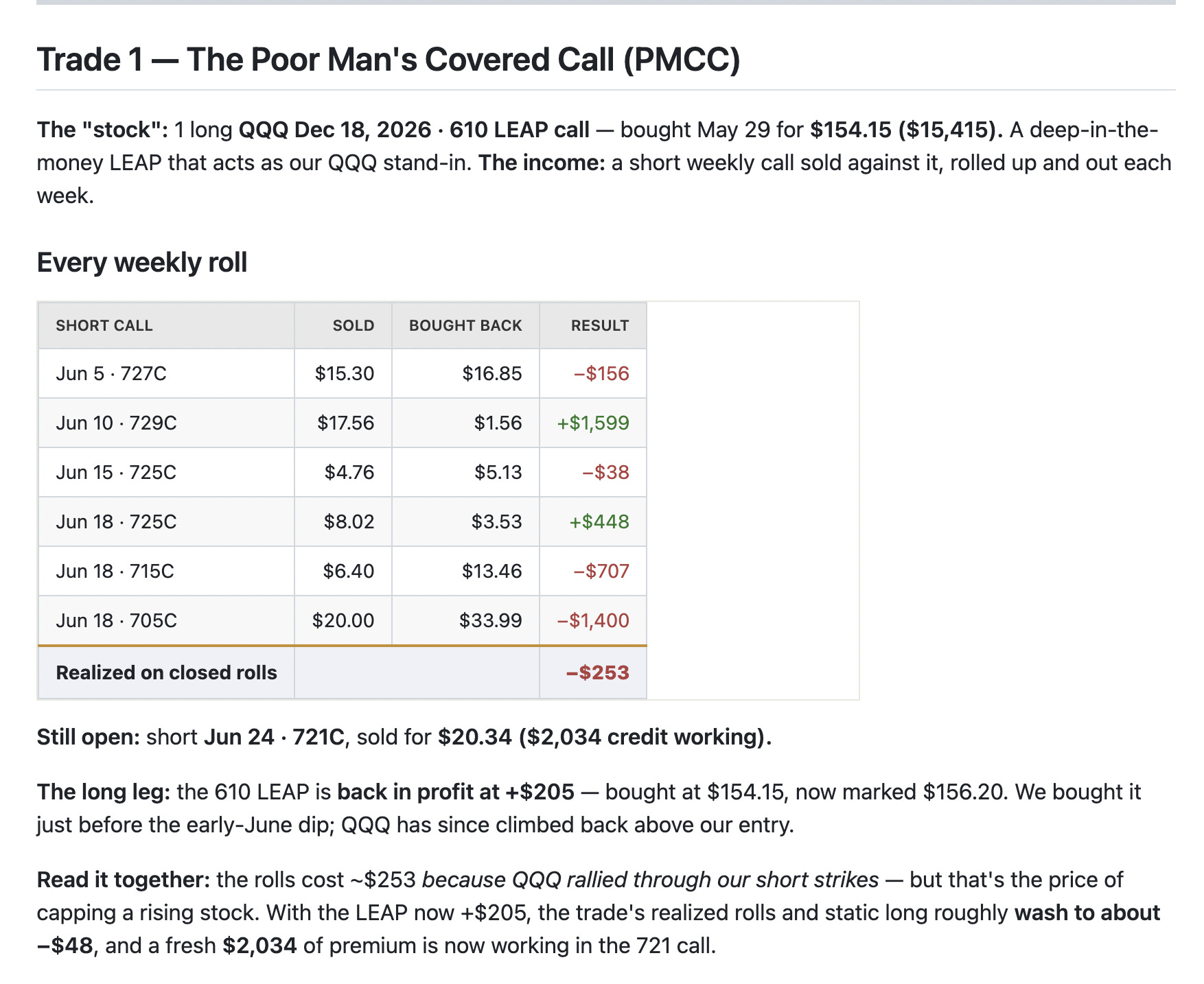

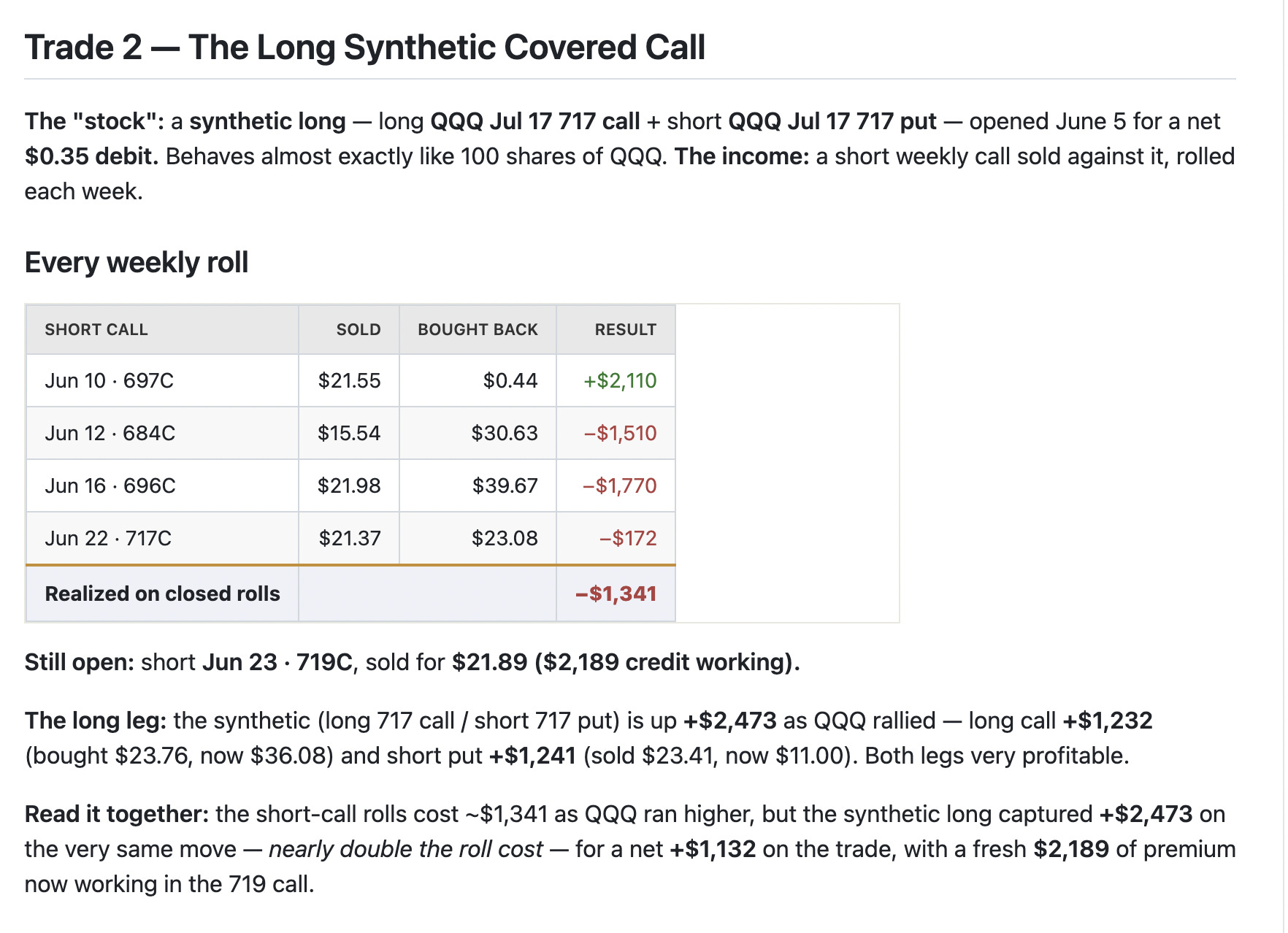

First, the one thing to understand before the numbers: a covered call is two pieces — a long “stock” leg and a short call sold against it. When the underlying rallies, the short call goes against you (you roll it up at a debit) while the long leg gains more. So the short-call roll P&L below, on its own, is only half the story — it has to be read next to the long leg. Both trades show this clearly.

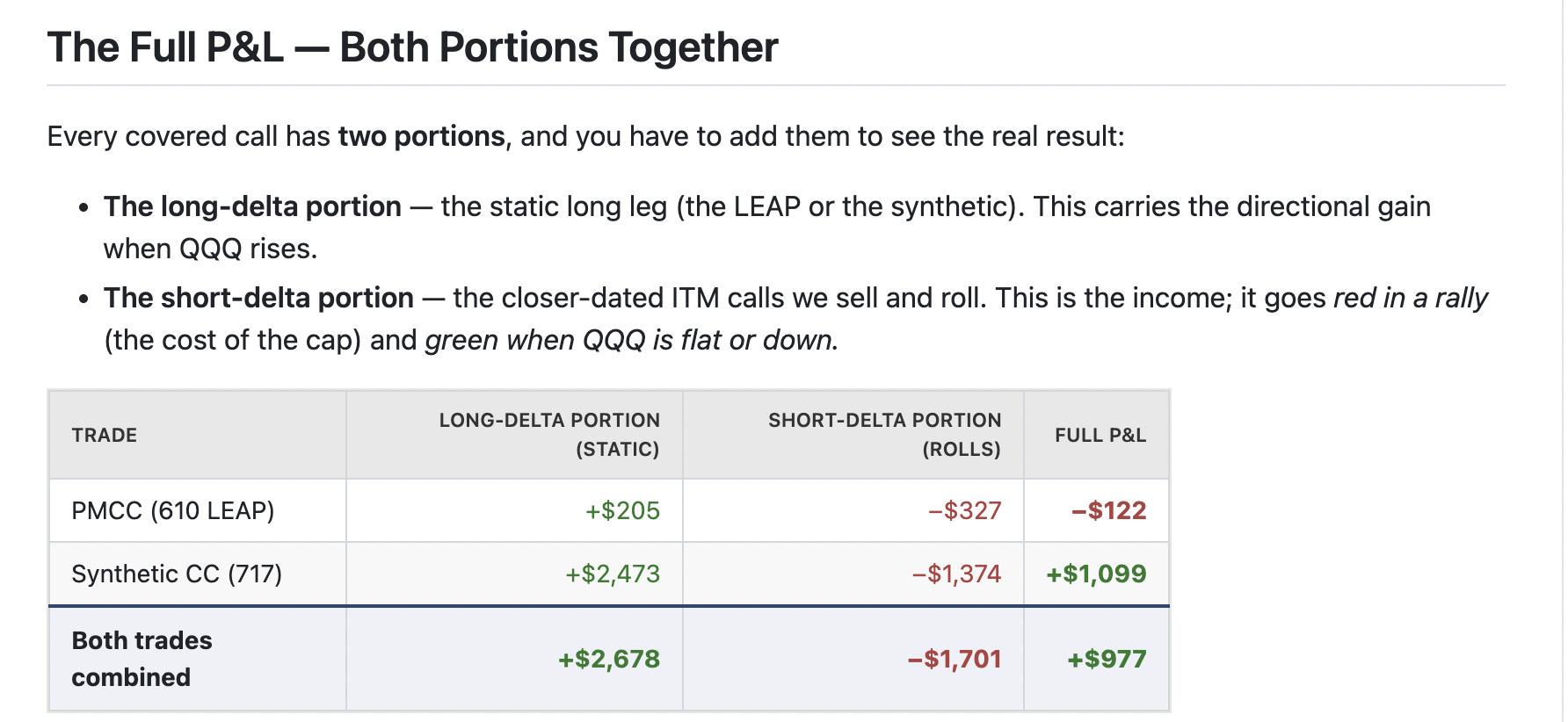

Short-delta portion = realized P&L on the closed rolls plus the current mark on the open short call (721 −$74, 719 −$33 — both opened today). All marks current: 610 LEAP $156.20, 717 call $36.08, 717 put $11.00, 721 call $21.08, 719 call $22.22; realized rolls from actual fills, fees included. The two open short calls still hold ~$4,223 of credit that decays in our favor if QQQ stays below their strikes.

The pattern is the textbook covered-call-in-a-rally: the short-delta portion is red (you capped a rising stock), but the long-delta portion gains more — the synthetic’s +$2,473 alone more than covers both trades’ roll costs. Counting everything together — the closed rolls plus every open leg marked to today — the two QQQ trades are net +$977, with another ~$4,223 of premium still working in the open short calls. You don’t catch the full melt-up, but you carry the move and keep compounding income.

The Lesson

This is exactly why we run these structures, and what TonyB means by “the goal is not to maximize any single roll.”