Trade of the day: $SPY Short Put

Got to Risk it to get the Biscuit !!

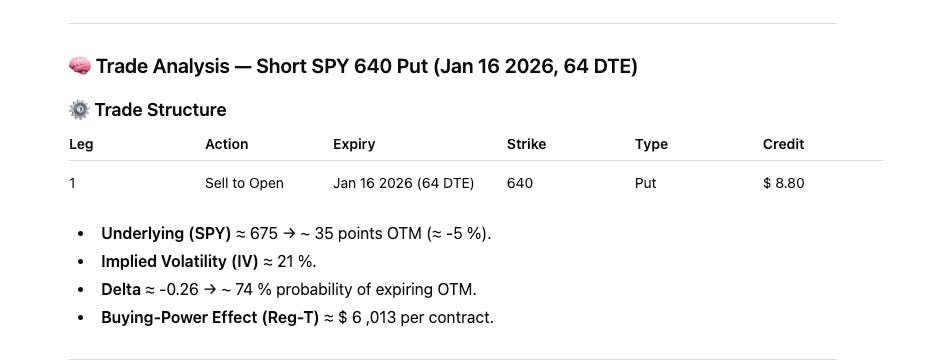

This trade is a short SPY 640 put, expiring Jan 16 2026 (≈ 64 days to expiry), sold for about $ 8.80 credit.Smaller Accounts can use SPY, /ES or /MES

This trade is a short SPY 640 put, expiring Jan 16 2026 (≈ 64 days to expiry), sold for about $ 8.80 credit.Smaller Accounts can use SPY, /ES or /MES